Trampling at Ath Pavura: Dissecting a Deal

You fool, I thought, as the social entrepreneur made his decision. He went for the smaller investment, resulting in a smaller valuation of the company, while foregoing the assurance of a client who would quadruple the demand for his product and profits.

A fortnight later, Dulith Herath, the unchosen ‘tusker’, reminisced:

Occasionally in life, we get an opportunity to help someone with so much potential. We can see what a bright future they have and they just need a little push and a little bit of funding to get going to do great things. This was one such occasion. Unfortunately, the candidate chose a different path. While I regret that he didn’t chose [sic] to walk with me, I respect his decisions and know he will do fantastically well.

Lankitha shared this on Slack with the Vesess team. Initially our consensus was that the entrepreneur failed to opt for the best deal. But did he?

Upon closer inspection, this little episode seems to reflect the same twists and turns of the bitter investor-entrepreneur drama we often see elsewhere, not just in social enterprises, and not just in Sri Lanka.

The following is our own interpretation of this investor pitch, deliberation, and the final result. We have taken the liberty of commenting, and perhaps projecting our own biases, based solely on what was shown on screen. We have not talked to the actors in this play, so our speculations might be off the mark: we apologise in advance for any misrepresentations.

Act 1: The Social Entrepreneur

Prabhath Amarasekera walks in. On the table by him are samples of the bags he produces. It’s clear that he is passionate about this venture. In fact, he still remembers the exact day the idea came to his mind: September 5, 2014. “Let’s avoid using plastics, let’s preserve the environment”—that’s his motto. He wanted to find an alternative for polythene bags, and had figured out that using non-woven fabric would be a good option.

His production capacity is 15,000 bags per month. The demand, however, exceeds 50,000. To develop his business to serve this demand, he needs an investment of Rs. 2.5 million, and in return he offers a 20 percent stake in the company.

The questions begin. We learn that Prabhath’s business has a monthly revenue of Rs. 800,000, and a monthly net profit of Rs. 200,000. He is a sole proprietor. His employees work from home: he provides them with material and transport, and pays them on a per-item basis. Prabhath did not have any capital to invest in the venture. The HNB bank in his area, Warakapola, had offered him a loan of Rs. 1 million to launch the business.

Prabhath has customers around the country. In addition to generic bags, he also offers branding and customisation. Compared with his competition, his prices are higher, but so is the quality: his large bag can easily carry 20kg of goods.

Before embarking on this venture, Prabhath was a school teacher. Now he is a full-time entrepreneur. During the weekends he conducts private classes at home to make ends meet.

Act 2: The Rejection

As it happens so often in Sri Lanka, things go wrong for Prabhath due to the language barrier (and of course, the only language where this seems to matter is English). He understands the material name ‘non-woven fabric’ correctly, and even translates it properly to Sinhala, but his pronunciation is slightly off the mark. This seems to trigger doubt in one investor (Gamini Saparamadu) about Prabhath’s domain knowledge.

Gamini also points out that non-woven fabric is still a synthetic, non-biodegradable material. It’s not clear whether Prabhath already knows this, as he does not interfere with the comments: perhaps he remains silent out of deference to Gamini. The advantage of the product is in its reusability, which Gamini appreciates, and a fact understood by Prabhath too, judging from his responses. Nonetheless, Gamini withdraws, saying that he doesn’t see the social entrepreneur he wishes to see in Prabhath.

If Prabhath had pronounced ‘non-woven’ in an ‘acceptable’ manner, would he have managed to keep Gamini in the fold? It’s difficult to figure out from the short exchange, but I feel it would’ve helped.

Act 3: The Offers

Prabhath, however, manages to grab the interest of three other investors. Two of them, Chandula Abewickrama and Upul Daranagama, make a joint offer: Rs. 500,000, for a 20% stake in the company. Prabhath makes a counter-request: would they be willing to invest Rs. 1 million for 20%? It is rejected, but Chandula says they would be open for further investments, and this is but the first step.

Dulith Herath intervenes, and offers Rs. 1 million, for 35% of the company. Again, a request from Prabhath: would he be able to reduce the stake to 25%? Dulith points out that he needs 40,000 bags per month for his e-commerce business Kapruka: a threefold increase in business that he can bring to Prabhath. Considering this significant value he brings to the table, Dulith says he is not willing to go below 35%.

Choosing between these two offers is difficult for Prabhath. He is seen speaking to another person outside the room, apparently discussing which one is the better deal. I’m watching this, and I don’t see what the issue is. Go with Dulith, I shout in my mind, he clearly has the better offer! You get money and guaranteed additional business—it’s a no-brainer!

Prabhath returns, and opts to go with Chandula and Upul: Rs. 500,000 for a 20% stake.

You fool, I think. You naïve fool.

What Is the Right Decision?

I was talking to Lankitha about this pitch and result, and he pointed out that I was wrong. There was no deal to be made in the first place: Prabhath should have walked away. Run even.

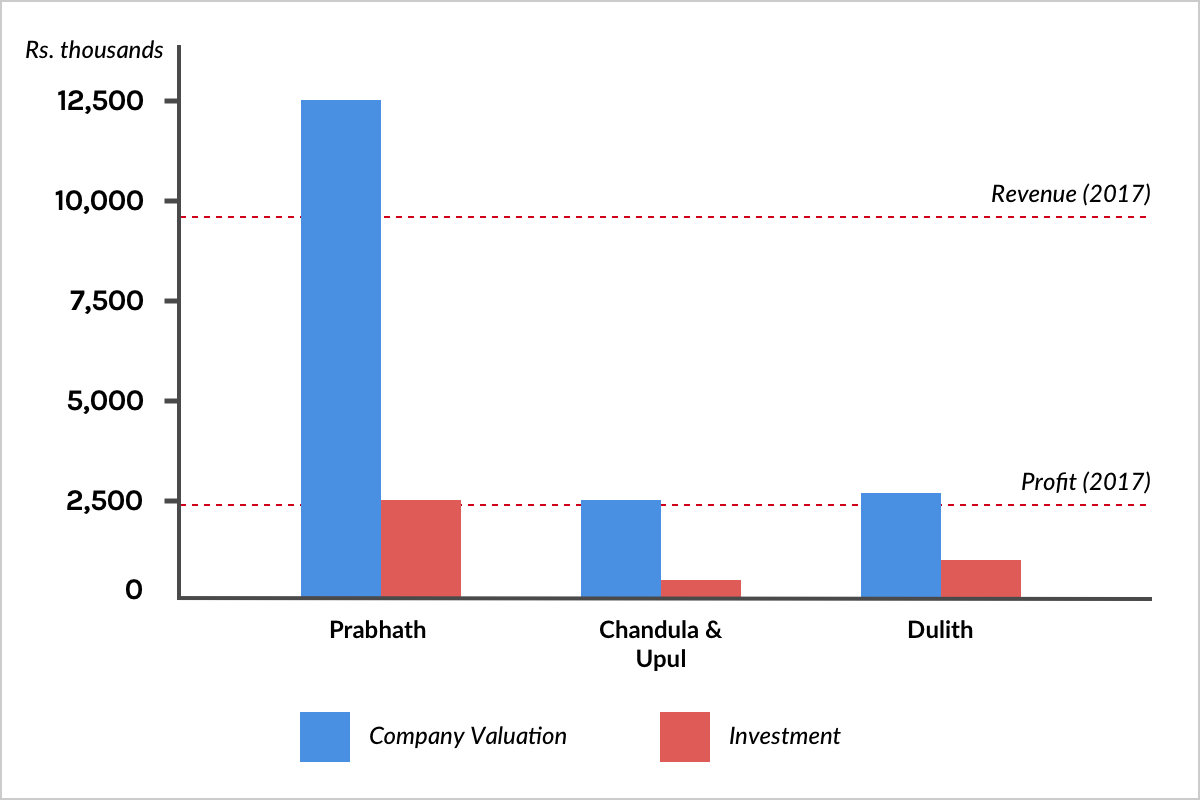

Prabhath came into that room with a company worth Rs. 12.5 million, and left with one worth only Rs. 2.5 million. By accepting five lakhs, he made another hundred lakhs disappear into thin air.

Now, one might argue that his Rs. 12.5 million valuation was mere entrepreneurial daydreaming, that it was not justified. But note that his business was making Rs. 8 lakhs per month (almost Rs. 10 million per year) in revenue, and Rs. 2 lakhs a month (Rs. 2.4 million per year) in net profit. Prabhath’s valuation of his company was just a tad above annual revenue, and only five times the annual net profit. His problem—the reason he was seeking investment—was to scale the company to meet demand that was three times more than his production capacity. Any reasonable assessment, based on the information shared with us, would value the company comfortably north of Prabhath’s own figure of Rs. 12.5 million.

Or frame it this way: how many months of net profit would you equate to a 20% stake in your company? According to Chandula and Upul—and Prabhath concurs—it would be 2.5 months. In terms of revenue? Less than three weeks!

But what about Dulith’s offer? It’s marginally better: instead of Rs. 2.5 million, Prabhath’s venture would be worth Rs. 2.8 million—needless to say, still a far cry from Rs. 12.5 million. Prabhath would then end up with a powerful investor + customer hybrid who would control 35% of his company and 80% of his sales, for an investment worth just 5 weeks of revenue.

Selling to a single customer might seem like a convenient way to grow a business, but it’s clearly riskier compared to a diversified clientele, one which Prabhath seems to be building already. Furthermore, it is highly likely that his profit margin off that 80% of sales to a single customer would end up being less than the usual 25%. Is all this trouble, devaluation, relinquishment of control and losing peace of mind worth it when the current demand is already way more than his production?

Here’s a handy visualisation of the ignominy of this whole situation:

I wish Prabhath walked away to bootstrap his business, like he has done for three years already. But he didn’t, and I guess he has good reasons. One can’t help but wonder: why would an evidently successful entrepreneur give up so much control of his venture for so little? Is this an indication of how desperate the funding scene is in Sri Lanka?

There’s no doubt that initiatives like Ath Pavura are to be promoted and supported (and we have already done so in this blog), but it is also important to point out bad deals when they are made. We can learn from them so that future entrepreneurs will be able to avoid these mistakes. And where possible, we can improve on them, to create funding opportunities that are more entrepreneur-friendly. This is the thinking behind our Vesess Alpha and Beta initiatives. At the moment these are limited to students in the tech sector, but we are open to expanding their domains in the future so that we may reach people like Prabhath as well.